Type 2 Fun and Investing Lessons

$CRWD, $JD, $AMZN, $GOOG

I can’t remember specifically when the term “type 2 fun” was first described to me, but I certainly have vivid memories of my encounters with it. There was camping in college when the Katrina storm path rained sideways for two days, completely soaking every article of clothing and gear my group had. There was backcountry skiing in Alaska when returning to the RV hours after sunset and needing to bushwhack through endless acres of alder bush. Or the time I badly rolled my ankle on a trail run in the Pemigewasset Wilderness, 10 miles from my car, with thousands more rocks to navigate.

The fun scale, with origins from the outdoor/climbing community, has three distinct tiers. Type 1 is what most seek when doing something outside – enjoyable and fun in the moment. Think spring skiing in sunny t-shirt weather, hiking with family, or paddle boarding on a serene lake. Type 2, on the other hand, is often challenging and miserable in the moment, but fun to reminisce about later. Ultramarathons and extreme mountaineering might be intentional activities that fall into this category. But often it’s other variables – weather, group dynamics, or poor luck – that lead a regular activity into the type 2 zone. These endeavors ultimately come with opportunities for reflection and self-improvement, but leave you excited to try again sometime in the future. Type 3 fun, on the other hand, is when something goes terribly wrong that you never want to repeat again. This might entail a rescue evacuation or permanent injury. For a wonderfully written but tragic piece about avalanches and tail risk, see this Morgan Housel piece.

Often your confidence will rise when things are going well (investing or outdoor pursuits) but this is also the time when caution may be most warranted. Conversely, when the portfolio has been going through a rough patch, and conviction has deteriorated, this may cause you to react emotionally or have an exaggerated blind spot and miss opportunities. Fighting overconfidence, through humility and steady temperament, while remaining curious and open to new ideas is a great middle ground to strive for.

The last couple years have been challenging for my portfolio. A lot of type 2 fun you might say. Much of it is macro driven - global pandemic, wars, interest rates, etc. But a lot of it is inherent in my decisions – extreme SaaS valuations, chasing trends, stepping beyond (trying to expand?) my circle of competence. But I hope there are lessons in there as well. Ironically, my top four individual positions are the same as they were at the end of 2021. Perhaps this is a sign of maturity – making fewer changes and being comfortable enduring the volatility inherent in a concentrated portfolio. Or perhaps I just haven’t been turning over enough new rocks that piqued my interest. Here is quick look at the top four.

CRWD:

Crowdstrike ($CRWD) is my single largest position. Shares were bought in late 2019 and throughout 2020 at prices far lower than today. I first wrote about the company here in 2021. Although the price is nearly the same today as two and a half years ago, it was not a smooth ride. It went up 40%, then proceeded to drop 65%, before doubling this year. Much of this fluctuation is valuation driven – the forward EV/S multiple peaked during the SaaS mania in the 40’s before dropping to 8 by the end of 2022. Regardless, the business has continued to execute. ARR has risen from $1.2B to $2.9B while the growth rate has slowed from 74% to 37%. Free cash flow margins have remained steady in the low 30’s. The unit economics have remained phenomenal – gross revenue retention at 98%, cost to book ARR at $1.05 (has risen somewhat as they move down market), and cost to service ARR at about $0.50.

The company recently laid out some very impressive projections for their next chapter as they push to become a dominant cybersecurity platform for the future. This includes tremendous growth in the emerging modules of LogScale, Identity, and Cloud, proving they are more than just a traditional endpoint company. The company anticipates those modules will be 50% of ARR in 5-7 years, up from about 20% today. From a financial standpoint, they set a $10B ARR goal in 5-7 years and raised the FCF margin target to 36% at the midpoint. This will be driven by improved gross margin and operating leverage in S&M and G&A, not R&D, which indicates to me the goal for continued product development.

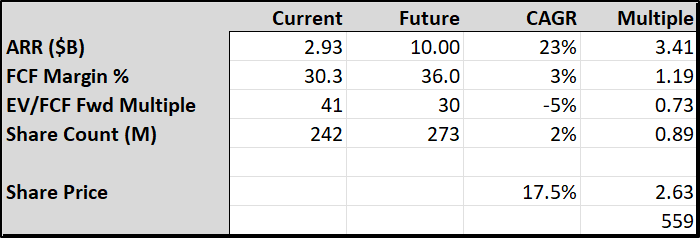

So, the question I should always be asking myself is what the IRR going forward is from here? Well with a company at a 2.5% forward FCF yield, the stock certainly is not cheap. But Crowdstrike is emerging as a winner (there remain several strong competitors!) in a secular growth market with tremendous tailwinds. Yes, the stock will constantly be fighting multiple compression and dilution, but it can still work. Using the John Huber three engines concept I pencil out a 2.6X return (17% IRR) over the next six years which equates to a stock price in the mid $500s. This is driven by a 3.4X in revenue, a 20% bump in FCF margins, a 27% decline in FCF multiple, and 2% annual dilution. See the summary table below. This does not include the ~$10B in FCF that would be generated over that duration. This will require tremendous execution, but Crowdstrike has yet to make any big missteps since becoming public. And while a 30X FCF multiple may still sound steep, the SaaS peer basket of CRM, ADBE, NOW, and WDAY currently averages a 31X forward FCF multiple with a 15% projected growth rate.

JD.com:

JD ($JD) is my second largest position with shares having been bought at a range of prices from 2018-2021. 2023 has frankly been a disaster as the shares are down 50% this year. JD is the second largest ecommerce platform in China behind BABA although PDD is quickly gaining on them. Revenue growth had ranged 20-30% annually from 2017-2021, before slowing to 10% in 2022 and a meager 2% in 2023 Q3. Known for their reliable logistics and authentic products, the retail segment has recently hit 5% operating margins, and the company will top $150B in revenue this year. JD has an enviable negative working capital position – they turn over inventory every 31 days while taking 53 days to pay suppliers.

While strict covid shutdowns somewhat stalled the Chinese economy the past couple years, there is also a looming demographic crisis as the Chinese population is forecast to drop by 50% by the end of this century. My initial thesis in buying JD was to own a dominant ecommerce platform company in a fast-growing economy where consumption would expand as the nation modernizes. While much of that still holds true there are some other headwinds. Ecommerce competition in China is fierce, and while JD has succeeded in battling Alibaba, there are emerging competitors in PDD, Douyin, and Kuaishou. JD has struggled to succeed outside of China and growth domestically is now focused on services and down market on lower value items. Additionally, I underestimated the political overhang of owning a Chinese company. In the past couple of years this has put tremendous pressure on valuations. Just consider that Alibaba IPO’d more than 9 years ago, and revenue is more than 10X since then, and the stock is still below the closing price from the IPO day. Even the secondary listing on the Hong Kong exchange for JD in 2021 has not done much to alleviate this valuation pressure.

With $33B in cash, and under $10B in debt, JD has a fortress balance sheet. Even with netting out the inventory and payables, JD trades at about a 5X EV/FCF multiple using $5.4B in trailing FCF. For a no growth but stable company in the US, I’d peg fair public market value more in the 8-10X FCF range. That is 60-100% upside right there, not to mention that analyst projections have EPS growing over 10% annually the next few years. With growth slowing and a strong balance sheet, the company has adopted an annual dividend policy. $3B has been returned in the prior two years. My hope is priority would focus on share repurchases (they have bought back over 20 million ADS units since 2020), but at least there is some acknowledgement of needing less cash for future investment.

AMZN & GOOG:

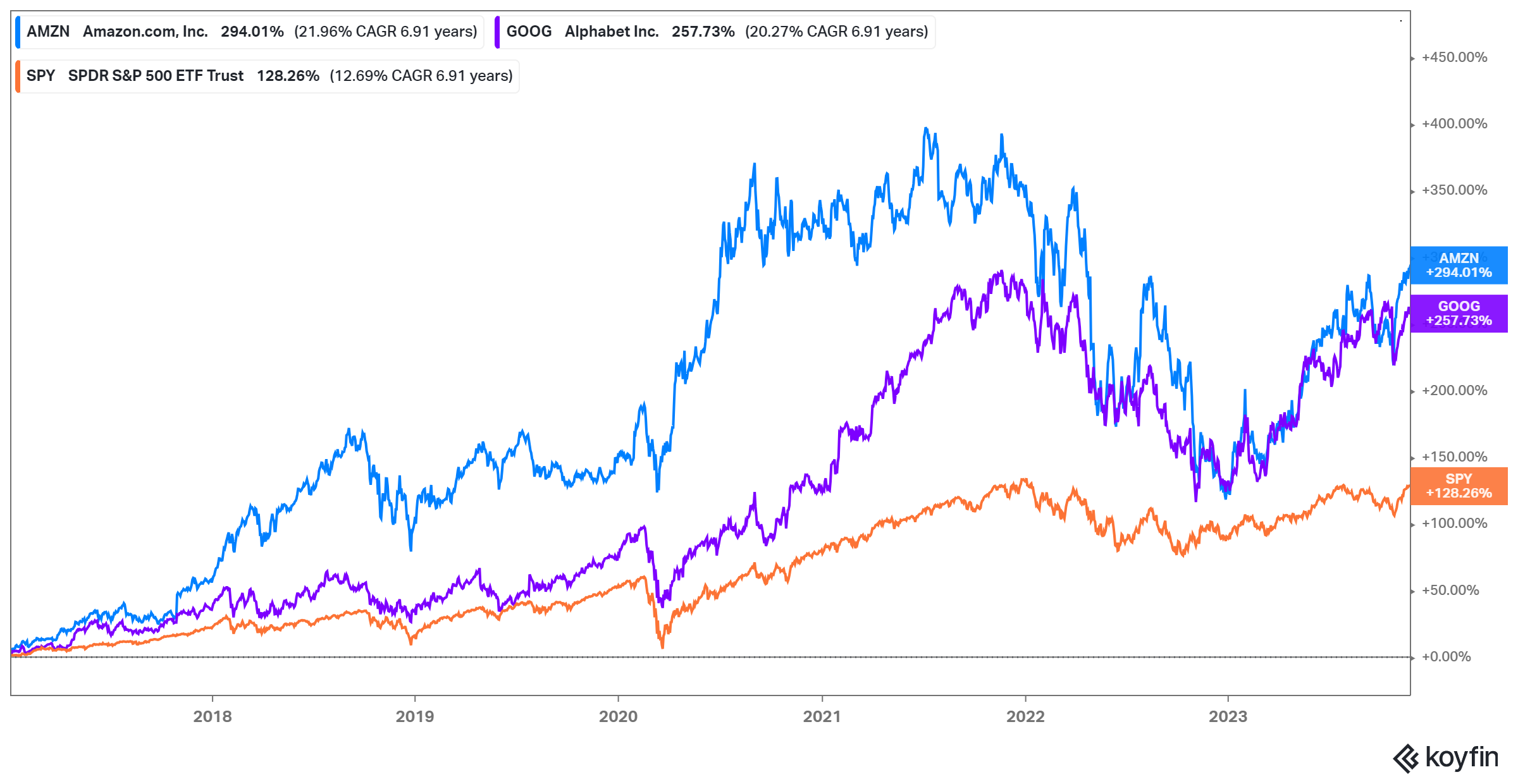

Amazon ($AMZN) and Google ($GOOG) are two of my older positions and have oscillated between third and fourth position in the portfolio. Amazon shares were bought in 2016/2017, while Google shares were bought in 2016/2017/2019. They have been solid holdings for the portfolio as they have provided about twice the return of the S&P500 over that period.

Normally labeled as big tech, they also offer exposure to retail, advertising, and media. So, I view them as diverse individual holdings that are better than owning index funds. They have strong growth prospects, innovation optionality, superior business models, and reasonable valuations. Recently there have been antitrust concerns brought against both Amazon and Google. Although I have not followed the proceedings closely, these are two of the greatest consumer friendly companies in society.

Google is essentially being challenged on the slotting fees they pay to be the default search engine on various smartphones, namely the iPhone. This was a staggering $26B in 2021. But some research (see this video from Polen capital) indicates that if given a choice instead of a default selection, and 70% of consumers choose Google, then the profit impact of eliminating the slotting is a wash.

The DOJ suit against Amazon is focused on the retail business, not the AWS cash machine. And the DOJ is trying to contend that there might be monopoly type abuse because Amazon has become a dominant ecommerce retailer. But all major retailers are becoming omnichannel, with ecommerce offerings, and when the true market share is retail, Amazon is still low single digit market share. I also think trying to frame the prime bundle as egregious and unfavorable for consumers is just ridiculous. Amazon has been a pioneer in customer value and convenience.

It clearly is no longer day one at either Amazon or Google, but the businesses continue to hum along. Google continues to see core search/advertising growth and owns arguably the most important video platform for the future in YouTube. While Google Cloud growth has slowed and margins are less than peers, the company has finally put some focus on their cost structure and continues to cannibalize their shares. Amazon invested tremendously at the pandemic onset in logistics infrastructure and the retail business is starting to see the leverage of those investments as NA operating margin hit nearly 5% in the most recent quarter. With continued growth in AWS and advertising the consolidated business is not far away from double digit operating margins.

Lessons Learned:

A big and obvious takeaway from type 2 fun is the capacity to suffer. Often, you can’t know if an adventure will work out. But the planning, skills developed, mental fortitude and resilience are all wonderful attributes that allow for that capacity to suffer. Feedback loops are incredibly long in investing, which makes it more mentally challenging than other endeavors. Crowdstrike has worked out as a great investment thus far while JD has been a huge financial opportunity cost. Researching both enabled me to learn greatly and enhance my range in new areas of SaaS/cybersecurity, China markets, and ecommerce/logistics businesses. Having a well-researched foundation is critical for enduring volatility.

These two examples offer a clear dichotomy in the growth versus value debate (I personally despise the labeling but it’s natural). Buying Crowdstrike at 15X forward EV/S valuation in 2019 with negative GAAP earnings taught me how durable growth can outweigh valuation concerns. Additionally, the importance of truly understanding unit economics is paramount. JD, on the other hand, may still be a value trap at 5X FCF. I believe otherwise but time may prove me wrong.

Type 2 fun also enables a great mindset around seeing the big picture and not dwelling on the short term. While Google could do no wrong in 2021, the past year has seen them questioned on their positioning in artificial intelligence with the release of ChatGPT. But almost a year into the LLM revolution and search share has barely budged for Google. Not to mention their internal LLM research and improvements to Maps, Gmail, Cloud, and Search. If training LLM models is a function of quality and quantity of data, then Google remains in a dominant position for an AI driven world.

Amazon could do no wrong by investors in 2020 as the pandemic shifted many sales online and they spent prohibitively on capacity expansion to meet customer demand. In the ensuing year, as margins were pressured and growth mean reverted (albeit back towards the trendline), investors punished the stock. Amazon was down 50%+ from its 2021 highs by the end of 2022. But nothing really changed in the big picture – AWS continues to grow as IT workloads move to the cloud, the shift of buying going online remains a secular trend, and Amazon has latent margin potential masked by their tremendous investments. It took just a little bit of cost discipline and growing into their capacity in 2023 for the market to realize this again and shift sentiment.

I am sure there are many more parallels between type 2 fun and investing but these were just a few that popped to my mind. Hopefully this mindset is something I can rely on as I continue my compounding adventure.

Disclosure:

Not investment advice. I own shares in CRWD, JD, AMZN, and GOOG