Redfin - Take the red pill?

The brutally honest and entertaining Glenn Kelman, long-time CEO of Redfin, gave a TedX talk in 2013 called Take the Red Pill. The premise covers how he believes software companies should work on real-world verticals instead of just building software to sell to others. This integration, he claims, can have a more potent impact on the world while creating durable businesses. This choice of building pure software versus an integrated model is akin to the choice that Neo must make in the movie The Matrix – take the red pill or the blue pill? Neo can take the red pill and confront the real world and learn potentially difficult truths or take the blue pill and remain worry free but ignorant of the real-world problems.

Beyond the obvious color comparisons with several of its major competitors, Redfin truly did take the red pill. A pioneer in map based real estate search, the company made a bold move early on by using that technology and software background to build a residential real estate brokerage. This contrasts with Zillow who, historically, has monetized their website via selling lead generation to brokerages. The Redfin mission is to “redefine real estate in the consumer’s favor”. They hired real estate agents as employees with benefits, paying them based on customer satisfaction and closed transactions – a big deviation from traditional brokerages that hire agents as contractors and pay exclusively on commissions. They took dead aim at the industry by charging 1% to 1.5% commissions for home sellers, a step function difference from the typical 2.5% to 3%. Although the savings for home buyers are somewhat opaque, as Redfin gives home buyers a post transaction refund for some of the commission, this averaged $1,750 per homebuyer in 2020.

As someone who frequents the Redfin app and has been through a residential real estate transaction (although not with Redfin), I wanted to study the company. Seeing Bares Capital and Saga Partners add it to their portfolios in 2021 certainly caught my attention, as both funds are concentrated, long-term oriented, and seek out high quality businesses. One of my newer research strategies has been to scour old interviews and podcasts with company executives and there are certainly numerous ones with Glenn. He mentioned that ample time and energy goes into the prepared remarks for earning calls where key insights and information is conveyed. I figured reading these would be the best way to learn the Redfin story. The following attempts to cobble together some quotes, mixed in with a bit of analysis, to tell the Redfin story.

1. Differentiation:

“And this is our mission, in a sales-mad baloney-gorged world, to be the truth-teller, the fee-squeezer, the game-changer. Our idealism may not benefit stockholders over months or quarters, but we believe that over the years and decades it will deliver the best results.” – S1, July 2017

“We started this business focused on buyers because we invented map-based search, which was a website feature for buyers. But over time we realized that to be an effective broker we had to have an equal number of buyers and sellers and we are still not at that point.” – Q2 2017

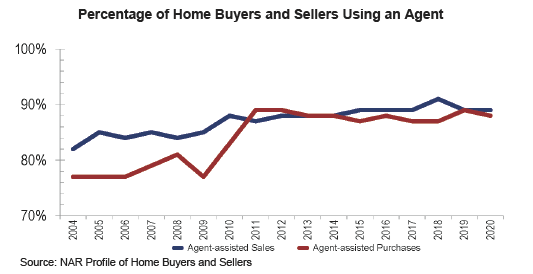

The residential real estate brokerage industry is very fragmented and has seen minimal technological change until recent years. The major legacy brokers of Realogy (Coldwell Banker, Century21, Sotheby’s), Keller Williams, ReMax, and HomeServices of America make up about 40% of the market. (Link) Newer entities targeted at recruiting agents – Compass and EXP Realty – make up 6% of the market as of 2020. And there sits Redfin in 8th spot at about 1% market share. I was a little surprised to learn that even with the readily available internet tools and portals for consumers to search for houses and research information, nearly 90% of buyers and sellers still use an agent. Perhaps this is just the nature of a major life and financial decision for a consumer, where having help walking through the process is valued.

Redfin’s major push to change the industry besides bringing a technology and consumer focus, was to cut the commissions rate and hire agents as employees. The national average for commission rates has barely budged in 20 years (link), although it’s finally beginning to feel some pressure. Redfin has already saved consumers more than $1B in comparison to a standard 2.5% commission on one side of the transaction. Having a natural lead generation funnel has allowed Redfin agents to be more efficient and attain higher NPS scores than competitors.

Hiring agents was not an attractive proposition to the venture capital community. Glenn claims he never met someone rejected more from venture pitches until he met John Foley of Peloton. Building an agent base with more fixed costs required sizing it correctly and growing at the right pace. To grow responsibly – not too fast but not too slow – Redfin refers some requests it gets to partner brokerages. This is typically in areas where Redfin has yet to develop an agent presence, or in areas where current Redfin agents are already fully occupied with customers. If a transaction occurs with a partner brokerage, Redfin will ultimately take 30% of the commission as a referral fee. This is how competitor Zillow’s legacy business has operated over the years – lead generation for real estate agents. As Redfin has grown though, the percentage of transactions done “in-house” has risen to about 80%.

Additionally, to effectively grow the brokerage business, Redfin needed to capture more interest on the seller side to combat the natural buyside funnel of interest from the website. This is where a radical commission cut can be a game changer, as the seller is often more price sensitive (buyer agent commissions are paid by the seller). From 2014 to 2020, the percentage of Redfin transactions from sellers grew from slightly over 20% to 44%. This helped developed a more well-rounded brokerage business and led to Redfin increasing national market share from 0.33% to 1.00%. The real estate services revenue over that time compounded at 29% annually.

Source: Redfin financial reports

2. Experimentation:

Throughout the course of Redfin’s history, it has been a constant iterative cycle of testing new concepts, collecting data, assessing the experiments, making changes, and rolling out ideas to different markets. This allows for the company to study a business strategy in isolation before wider implementation. A key example of this is the 1% listing fee for sellers. First launched in Washington DC a few years prior to IPO, the thought was that going after seller share might compromise share among home buyers. After realizing that was not the case – buyers were less price sensitive and increased seller share drove general brand awareness – it was rolled out to Seattle and a couple other markets to validate the findings. Another year later in 2017, the company was confident this pricing strategy was effective and therefore planned to roll it out everywhere.

In 2019 Redfin began testing 1.5% instead of 1% in seven markets but kept the 1% rate if sellers opted to use Redfin when buying a home in the next 12 months. Redfin believed that even at 1.5%, no other broker could offer comparable service and that listing share would continue to expand. Although the seven test markets experienced slower share growth than ones where rates were unchanged, the thesis was largely true. Gains from higher pricing more than offset slower share growth, but the real benefit was encouraging more sellers to use Redfin when buying. This allowed customers to get the best rates and facilitated two brokerage transactions for Redfin.

“As we experiment next year with lowering the number of homebuyers each Redfin agent serves, the gross margin impact will depend on whether more personal service leads to higher close rates.” – Q3 2017

Another key area that Redfin has constantly been tinkering with is balancing agent load with providing the best customer experience possible. In 2018, Redfin lowered the average number of homebuying customers agents served by 10% with the goal of increasing close rates. In a strong sellers market, agents had been clamoring for more customers even as close rates dropped. A year later Glenn claimed this was half a mistake and half beneficial. Positive in the sense that it reinforced to agents the positive habits of developing client relationships and strengthening Redfin’s overall culture of service. But partially it ended up being a mistake as many tenured Redfin agents grasped these concepts quickly and were capable of handling more load.

By mid-2019, Redfin had studied the whole cohort of 2018 website visitors who requested tours and saw that service improvements had been completely offset by the chances a prospective buyer bought any home at all, both at Redfin and other brokerages. This inefficiency can put tremendous strain on the brokerage gross margin. Redfin revisited this failure during the covid era, running a six-market pilot for 18 months testing 24% lower homebuyers per agent. While the closes per agent were obviously lower, the close rates per client were higher, with the service improvements yielding more sales and gross profit. Additionally, this recalibrated load showed signs of better agent satisfaction and retention, great for future margins. If this trend remains true throughout 2021, Redfin plans to roll out this new agent load nationwide by the end of 2022. Being adaptable to the changing market dynamics and constantly testing new strategies may be Redfin’s biggest strength.

“But our biggest competitive advantage isn’t what we did in the past. It’s how fast we’re reacting now. When the world is changing this fast, what is most valuable is our own ability to change. The company you want to stake in isn’t a big fat incumbent. It’s the crazy little mammal, crawling out of the crater of the asteroid strike.” – Q1 2020

In 2017 Redfin reluctantly launched a different kind of experiment, their instant home buying business called RedfinNow. Management was skeptical of the merits of buying homes outright from customers but saw the value in wanting to understand the market better than anyone else. A customer typically gets a lower price for selling the home but is rewarded with a cash offer, certainty of closing, a shorter timeline, and fewer potential roadblocks. RedfinNow launched in Southern California with a $10M capital limit to experiment in the market. A year later, the company proved even after labor, renovations, and capital needs, that it could break even. Making the push into a full-fledged business required hiring more software engineers to create tools for engagement, pricing properties, and managing renovations. And each additional market area introduction required developing local field operations.

But the real revelation for Redfin in their iBuying experiment may have been learning how much it can help the core brokerage business. When presenting an offer to a home seller, Redfin could come in with information about what they thought the house could sell for under a traditional sale, presenting the customer with both options. Many opted for the traditional route, teaching Redfin this was a good tool for building out the entire Redfin ecosystem. Also, understanding the dynamics around why a customer would take an instant offer (liquidity needs – can’t get two mortgages, timing, etc.), showed Redfin a future where they could use data and information to help customers potentially get bridge financing and avoid needing a capital middleman.

3. Integration:

“But we also believe that listing search, brokerage service, mortgage, title, instant offers, and renovations are more than the sum of their parts and that we can, over time, combine these services in ways that let our customers buy and sell homes other people can’t.” – Q2 2019

According to tech investor Keith Rabois, “the formula for startup success: find a large highly fragmented industry w low NPS; vertically integrate a solution to simplify the value product.” Redfin certainly set out to tackle a difficult problem and make it more consumer friendly. But the next evolution has been to integrate all aspects of the transaction and enhance customer choice. The core brokerage business will only get stronger with the development of ancillary businesses – Title Forward, Mortgage, and RedfinNow. Consumers tend to prefer a simple process and dealing with fewer entities eases the stress and streamlines the process.

Title Forward, which offers title and settlement services, started in Pennsylvania in 2012 and now operates in 27 markets across 14 states. Redfin Mortgage started in Texas in 2017 and has rapidly expanded across the Redfin network. It now geographically covers 81% of brokerage buyers and expects to cover 94% by year end. Redfin Mortgage is purely an originator that then sells loans to third party investors. It has seen rapid growth, from just 42 loans in 2017 to over $800M in loan value originated over the past four quarters.

Glenn has said that long term the Mortgage and Title Forward businesses should have similar margin profiles to the brokerage business. Title services tend to be less competitive, although this may be changing, and Redfin believes a 50% attachment rate is attainable in the future. Consumers are much more price sensitive and shop around for mortgages so 25% is the realistic goal there. Mortgages all come from the buyer side though, so a 25% attachment rate implies 50% on the buyer side if the buyer/seller transactions are equal. Recently, Redfin Mortgage has been running at about 4.4% buyer attachment rate (~2.4% / ~55% buyer transactions), so there is clearly a lot of room for growth. And this does not factor in the potential for capturing mortgage customers outside of the brokerage business.

Note: Attachment Rate = Origination of loans held for sale / 77% of real estate transactions value. NAR survey data reports show that from 2017-2020, 86-88% of buyers use financing, and for those who use financing, 87%-90% of the home value is financed on average. 77% comes from 87% x 88% = 77%.

“Mortgage, Title, RedfinNow is like compressing a string, straining our income statement and our people. But if and when these businesses pay off, our expectation is that the spring won’t just return to its former shape, but launch the company into a new competitive position.” – Q4 2018

As Redfin works to integrate these businesses together it should offer an even better value proposition for consumers. Consumers want simpler transactions with fewer counter parties involved. Having the best solution with the best price under one entity will be extremely valuable for Redfin. Customers coming for a single solution may become aware of the full suite of offerings and therefore think to use Redfin more in the future, creating a future uplift in demand for services.

Another key integration for Redfin has been their push for data transparency and information democratization. Redfin launched their home value estimate tool – Redfin Estimate – in 2015, becoming the first broker to do so. They claim it is the most accurate in the industry, but I am sure the iBuyers would argue that. Redfin bought Walk Score in 2014 which quantifies and assesses the walk ability of a specific location. This has since been expanded to include measures to assess the bike ability as well as public transit options for a given spot. But perhaps the biggest push recently is Redfin publishing buyer agent commissions wherever possible. This should put continued pressure on commissions and help consumers realize the Redfin value proposition. Pushing data integration, along with growing more share of sellers, will help develop some of the newer Redfin initiatives. These includes concepts like Redfin Direct Offers (buy without a buyer agent) and Redfin Direct Access (tour listings without a buyer agent).

4. Brand Development:

“Most Americans still think Redfin is a website. And that drives me crazy because I want them to know that they could save $10,000 selling a house through us, get better service and get a higher price for the home. So that’s the message, not that the website is red or that it has better listing data or something like that.” – Q2 2018

Perhaps most disappointing for me in researching Redfin was realizing the general lack of brand awareness and value proposition amongst the public. Rival website Zillow has the mindshare dominance – it was parodied on Saturday Night Live and has viral Instagram accounts like ZillowGoneWild. But even realtor.com has higher unique monthly visitor counts than Redfin. Having recently passed Trulia (a Zillow entity), Redfin sits as the third most popular real estate website. Although it sits in third, Redfin has been growing visitors faster over the past five years and the ratios are narrowing.

Source: company financial reports

While having 50 million unique monthly visitors is impressive, the lack of awareness around Redfin as a brokerage, and not just a website, is concerning. Redfin historically surveys a lot of consumers asking them to list the first three brokerages off the top of their head that come to mind. They track trends in this as a measure of brand awareness. In December 2016, only 4% of consumers named Redfin. This grew to 8% in May 2018, and 10% in March 2019. What is interesting is that Redfin has been running various ad campaigns in different markets and through different mediums to track the efficacy over time. This gets back to their experimental and data roots. From 2015 to 2019, in markets where Redfin ran TV ads for five consecutive years the affirmative responses increased from 6% to 19%. (I suspect this might only be Seattle and DC, Redfin’s top two markets) For similar sized markets that did not receive TV ads over the period, the awareness metric only rose from 2% to 4%.

“What has been the most reassuring to learn is that a craft that once seemed to involve branding voodoo and a Taco Bell-size budget, in fact, works best with the same data driven, cost-conscious approach we’ve taken with almost every other major investment.” – Q3 2018

Clearly the return on advertising spend for the brokerage business is a long-term game. An individual decision to buy or sell a home is often years in the making. By spending to increase brand awareness, consumers learning about Redfin now may not contribute until years down the road. It took Redfin many years of studying this to really pull the trigger on brand investments. After spending only $4-$13M annually on mass media advertising from 2014-2018 in select markets, Redfin ramped that up to $39M in 2019 across many more markets. And after shuttering much of the spend during the early months of the covid downturn, the 2021 plan is currently for $52M in mass media spend, much of which already happened in Q2. Hopefully these investments help to grow awareness and build market share over time.

In early 2021, Redfin announced their first large acquisition, buying RentPath for $608M. RentPath owns a variety of rental search websites (rent.com, rentals.com, apartmentguide.com) and will help Redfin create a more complete customer solution. The logic behind this purchase is to increase the breadth of customers entering the Redfin ecosystem, enhance the search experience (offering both buy/rent options), and to bring the Redfin touch to improve the rental experience. RentPath is quite nascent in the Redfin story so it will be interesting to see how this unfolds. But it will certainly help enhance the brand over the long term.

5. Competition

“We’re omnivorous. We’re going to try to take share in the big markets and in the small markets. We’re hiring everywhere. It’s like those bears you see in Yellowstone Park, they eat the garbage, the blueberries, they eat everything.” – Q2 2020

Redfin started the brokerage business in urban coastal locations and has slowly been spreading across the country. They now operate in more than 100 markets across 44 states. It has been a slow and steady march to the current 1.18% market share that Redfin occupies as of Q2 2021.

The legacy brokerage competitors (Realogy, Keller Williams, etc.) are the obvious area where share gains are possible, and they appear to be ramping their technology spend. Without an incumbent website and a natural lead funnel this appears unlikely to prevail. Mortgage centric companies like Rocket and Better have recently announced they are entering the brokerage business and may turn into interesting competitors. The iBuyers (Opendoor, Zillow, and Offerpad) are betting that building real estate services around iBuying will prevail long term. That may be challenging though as national share has yet to surpass 1% and even the top iBuyer markets (Phoenix/Raleigh) only hit 5-6% of market transactions during 2018/2019 before slowing rapidly during covid. The last couple of years have seen an explosion in two companies (Compass, EXP Realty) focused on attracting real estate agents through generous commission splits and revenue sharing arrangements.

“We are not going to grow 90% or 150% because we can’t hire enough agents to deliver fantastic service to every one of our customers through some kind of bozo explosion, where we’re hiring every single agent who can fog a mirror. Instead, we’re trying to hire the best people, deliver fantastic results to our customers. And that is going to limit our short-term growth but ensure long-term growth.” – Q4 2020

Although Glenn may be throwing shade at the viral growth of Compass and EXP, it’s worth looking at whether their business models are sustainable in relation to the Redfin customer proposition. Redfin reports how much they save customers in relation to a standard 2.5% commission rate, so their effective commission rate can easily be calculated. This could also be backed into by assuming the partner real estate revenue is 30% of the commission total. I have plotted what Redfin looks like over the past three years in comparison to some of the major competitors.

Source: company financial reports

Redfin has been around 1.9% before jumping to 2.0% in 2020, likely due to rolling out the national rate of 1.5% to sellers in Q4 2019. This was a fee increase for half of customers and a decrease for about 20% of customers. Some of the rise may also be a bump in seller use of Redfin Concierge – the service that fixes up homes in addition to the standard selling offering, and costs 2.5% instead of a 1.5% commission. It also important to keep in mind that the Redfin number includes 15-20% from partner transactions, so the true Redfin commission rate is lower than calculated here.

The real takeaway from the commission rates though is that the major competitors are all around 2.5%, which means Redfin has a rate about 20% less than them for comparable service. Could the competitors be profitable with 20% lower rates? 10% lower? The short answer is no. Realogy, the most mature operator in the space, has had operating margins in the 6-9% range over the past few years. EXP, which operates no physical offices, and offers generous revenue splits and recruitment bonuses has recently achieved 2% operating margins. Compass targets top real estate agents in higher end markets, offering them very high commission splits, and is working to build a real estate agent tech platform. But they have yet to break even, with an operating margin of -1% over the past 12 months. And there are rumblings that many agents who signed lucrative deals with Compass are waiting for multiyear contracts to end before leaving.

The battle across the real estate landscape is being fought through commission pressures, agent preferences, and technological change. I thought an interesting way to measure the strength of the Redfin ecosystem was something described by Nick Sleep is his fund letters as the “Robustness Ratio.” It is a framework he uses for quantifying the strength of a company moat and is particularly appropriate when the customer proposition is based on lower prices. The ratio is simply the amount of money customers save relative to the amount earned by shareholders. He shows how Geico was 1:1 in 2004 and how Costco works out to a 5:1 ratio. The higher the ratio, the more difficult it would be to compete with theoretically. You can also compare these numbers to potential employee benefits as they are a critical part of the business ecosystem as well.

Redfin has been reporting their customer savings relative to the standard 2.5% commission for some time now ($185M for 2020). They also cite quite regularly that their lead agents earn twice the median agent pay from the national NAR profile. This should get adjusted, however, as Redfin agents tend to operate in metro areas with much higher real estate values than the national averages. Using two different methods (per capita income by metro area, and home sales price data) I was able to figure that Redfin agents should be compared to something 20-30% above the national median pay. Figuring the amount shareholders earn is a bit of a theoretical exercise as the allocation of operating expenses to brokerage are not disclosed and there are a lot of growth investments going through the income statement currently. Deducting advertising costs, half of technology spend, and 5-10% of G&A (for non-brokerage businesses), yields operating margins ranging 6-15% over the past four years. A very simple assumption can be to just use a normalized operating margin for the brokerage of 10%. Again, theoretical exercise here.

Compiling all the calculations, I find that Redfin had a strong robustness ratio of 3.4 in 2017 which has dipped slightly to 2.8 in 2020. Most of the benefit in the ecosystem is still going to the customers (65% in 2017, 60% in 2020), while the aggregate benefits have been growing at a 18% CAGR over four years. Sleep also explains how earlier in a firm lifecycle, more of the benefits should be allocated to customers to induce loyalty, referrals, and building a valuable franchise. Over time, shareholders can expect to gradually take a bigger portion of the pie.

6. Future:

“I’ve never worked so long in a business where there are still so many ways for it to grow.” – Q4 2017

“This is why we believe we can build a company an order of magnitude larger than the one we have today.” – Q2 2021

“…but mostly as with all our market shares gains, it’s an inexorable march. I think we’re going to take more and more share whenever we focus on something that’s what we do.” – Q2 2021

It appears inevitable that Redfin will continue to take share, but at what rate, and at what future margin potential is a giant question mark. As the elite vertical integrator in real estate transactions, it remains to be proven if they can become more prominent than the legacy brokers, the iBuyers, and other website competitors. I envision a few different scenarios for where they might be in 10 years:

Base scenario: continue to gain market share at about 0.125% per year. This is about the rate they have gained share in the previous five years. Assume real estate inflates at 4% annually and Redfin maintains a 2% effective commission rate. Assume mortgage attachment rate hits 7.5%, title attachment rate hits 20%, and RedfinNow as a percentage of regular real estate services transaction values hits 3%. (Highest ever quarter thus far was ~1.3%)

Bullish scenario: continue to gain market share at 0.25% per year. This is approximately the rate Redfin has gained share the last two quarters and is their highest ever. Assume real estate inflates at 4% annually and Redfin maintains a 2% effective commission rate. Assume mortgage attachment rate hits 12.5%, title attachment rate hits 35%, and RedfinNow grows to 6% of real estate services transaction values.

Blue-sky scenario: Redfin brokerage hits 8% market share in 10 years to $10B+ revenue. Mortgage attachment rate hits 20%, title attachment rate hits 50%, other revenue is $2B+. RedfinNow grows to 10% of brokerage transaction values and hits $50B+ revenue.

Assigning a valuation to these future scenarios requires a lot of guess work (use whatever margins and multiples you want) but I put some numbers in the table above. Keep in mind that the exit growth rates will likely be lower than the CAGR over that time period in all scenarios. The base scenario implies no return over 10 years, that Redfin is unable to gain much traction, and that the company ultimately is not valued much more than a standard real estate brokerage. The bullish scenario implies a more market level return (~10% IRR) and higher profitability of RedfinNow. The blue-sky scenario is where Redfin gains real traction, the software efficiencies build on themselves, and the company receives a valuation for becoming the new age real estate platform. The dispersion of outcomes here is so wide that it’s difficult to even assign probabilities although scenario #2 seems most likely to me.

Writing up the Redfin story made it clear I am not ready to take a position, but I like a lot of what they are doing in real estate, and really appreciate the company ethos. I wish I could make the plunge and take the red pill now, but I am not quite there yet. The most important things to track going forward are the continued market share gains in the brokerage business, new innovations/disruptions to the brokerage business, attachment rates for other services, and the general unfolding of the iBuying market. I find it difficult to believe iBuying will ever gain a substantial market share, but if so, the vertical integration and customer focus of Redfin will prove extremely valuable.

Disclosure: not investment advice