Progyny

Ample tailwinds, debatable moat

In my quest to find secular growth stories outside the technology realm that can be win-win-win scenarios, I started an investment in Progyny (PGNY 0.00%↑) earlier this summer. It’s still quite small (<2% position) as I continue to learn, research, and gauge the potential for this investment.

Progyny is a fertility benefits management company with a mission “to make dreams of parenthood come true through healthy, timely, and supported fertility journeys.” Currently, only 50% of large employers cover some type of fertility benefits in the US but this has risen in the past decade. The benefits offered by Progyny are a small subset of a health plan typically offered by an employer. Their clients are major self-insured enterprises (led by big tech) and currently include 273 companies in a range of industries covering over 4.2 million members (employees plus partners on health plan).

The Problem & Progyny Offering:

Infertility is a massive problem in this country. According to the CDC, 1 in 8 couples struggle with this condition. Its root cause is varied - female reproductive issues (e.g., diminished ovarian reserve, tubal factors, endometriosis), male factor issues (sperm motility or production), or an unexplained combination of reasons contribute. While treatment for infertility has been around and improving over the past four decades, it has traditionally not been covered by most employer benefits packages. With high out of pocket costs and uncertain outcomes, it therefore has been primarily used by couples in the upper income brackets.

Conventional coverage has been designed to limit costs and utilization, often to the detriment of employees and employers. These include mandated step therapies (often lower success procedures first like IUI), lifetime dollar maximums (leaving members with difficult decisions and more expenses), and not covering advanced diagnostics (like PGT-A testing). These policies often lead to poor outcomes such as lower live birth rates or higher risk of miscarriage or multiple births. Not to mention the immense financial, emotional, and physical stress put on those going through infertility.

Progyny found their niche by combatting conventional coverage and were greatly aided by two of their earliest clients – Google and Facebook. Working with these two, who are innovative and forward-thinking employers, they were able to force the national carriers to integrate the Progyny system of focusing on outcomes. This process uses the best course of treatments and latest technology available. They do this via their Smart Cycle approach, which designs different treatment options but ensures at least one full course of IVF (egg retrieval and embryo transfer). Most employers offer multiple Smart Cycles of coverage (typically 2-3), while some cover additional cycles if the prior ones are unsuccessful. Different options within the Smart Cycles allow fertility specialists to try the best course of treatment for each situation and does not apply the “one size fits all” protocols that often disappoint.

Progyny essentially acts as a customer service layer between the employer, members (employees and partners), and the fertility clinics. Each member using Progyny is assigned a dedicated Patient Care Advocate (PCA) to help guide them throughout the process and provide support. Members have been very satisfied with this high touch offering, with NPS scores around 80 for both the benefits and integrated pharmacy offering. There is clear tangible and intangible value provided to all facets of this ecosystem:

Employers: Higher success rates lead to savings in fertility treatment costs, while superior clinical outcomes lead to savings in maternity and Neonatal Intensive Care Unit (NICU) costs. Integrating with Progyny Rx also leads to 10-20% cost savings. On the intangible side, employee retention, attraction, satisfaction, and absenteeism are greatly improved. If properly accounted for these translate to significant savings.

Members: With the Smart Cycle system providing comprehensive coverage the financial overhang is greatly reduced. There is improved access to the premier clinics across the country. And the better chances to build a family are an immeasurable benefit.

Clinics: Taking patients who are fully covered offers lowered financial risk, while enabling them to use the best treatment protocols and produce better outcomes. Progyny, as an aggregator, streamlines the administrative work and enables data sharing and reporting to track clinics, which helps them develop best practices.

Tailwinds:

There are several societal tailwinds backstopping the Progyny story. Fertility is often driven by female age, as chances for success start to decline in ones 30’s. This article references monthly odds of natural pregnancy for those couples actively trying as 20% for a 30-year-old woman, and steadily dropping to less than 5% for a 40-year-old woman. Also complicating this factor is that egg quality really drops off by the mid 30’s leading to higher risk of chromosomal abnormalities, which can cause miscarriage.

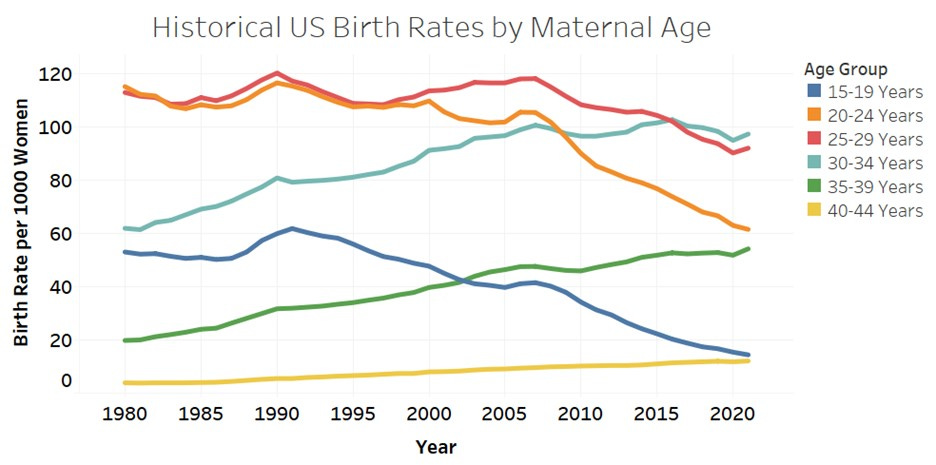

Women are waiting longer in life to have children and that trend seems to be unstoppable. Women now represent 60% of undergraduates at US colleges while career development and financial stability have become more of a focus prior to starting a family. Data below from the CDC indicate that even with a declining total birth rate in the US, the rate for the over 35 cohort has tripled since 1980.

Another major tailwind supporting assisted reproductive trends is the proliferation of LGBTQ+ individuals. A Gallup poll from this year indicates the percentage of US adults who identify as LGBT to have risen from 3.5% in 2012 to 7.1% currently. The rise in the younger generations is even more drastic. Millennials, the current family forming generation, has gone from 6% in 2012 to 10.5% currently. While Generation Z, the next family forming generation, has gone from 10.5% in 2017 to 20.8% this year. While not medical infertility, these populations need access to fertility services such as surrogacy, donor egg/sperm/embryos, IVF, and adoption for family building. Progyny makes it very clear that equal access to Smart Cycles, even for populations not historically covered (such as single parents by choice), is part of the program.

Along those line, many companies are eager to pursue fertility benefits as part of their DEI and ESG strategies. In the competition for talent, companies are viewing benefits as key differentiators. They often feel pressure to cover fertility once peer companies implement them. So not only will more people need fertility services in the future, but more companies will also cover it as a benefit. From Chairman David Schlanger on a recent podcast –

“In an environment where women have been discriminated in the workplace for decades, companies have not been viewed as family friendly. And if you don’t cover fertility, I think you’re making a very negative cultural statement about who you are as a company, that you don’t really value your female workforce. Because fertility treatments are uniquely borne by women. Men don’t get IVF, women do. If you don’t cover fertility, I think you’re making a negative cultural statement about where you stand about people having families. Whereas on the flipside, if you do cover fertility, and cover it in a robust manner, and encourage your families, when it’s your time, have a baby. I think you’re making a pretty strong cultural statement about who you are as a company. You know, how you view your role in the community and what health care is really all about. So, companies get that. And because our benefit is inclusive, you can be a same sex couple, they want to make that statement to the LGBTQ+ community also that they’re an important population and they’re going to provide them important benefits that allow them to build their families also, because those populations have family building dreams too.”

Finally, as these tailwinds encourage more coverage of fertility benefits and the medical outcomes continue to improve, more of the potential users of these benefits will be unlocked. Developed countries such as Japan and Australia have more than 2X the percent of babies from IVF than the US, while the highest – Denmark and Israel – are more than 5X. More recent developments of offering egg freezing and encouraging more genetic testing foreshadow a more preemptive future strategy to fertility than reactive, something that could benefit Progyny for a long time.

Revenue Quality:

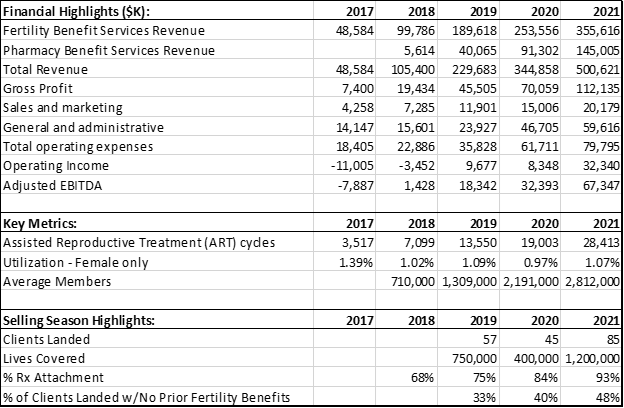

Will Thorndike, author of The Outsiders and creator of the new podcast 50X, outlined some attributes of revenue quality that correlate to persistence in great stock returns. Recurring revenue with low gross churn is a key factor. Progyny certainly fits this bill. While they often tout “near 100% client retention” in all their presentations, I have been able to identify three clients that have left for a different provider. Red Bull in 2021, and both Activision and Lyft in 2022. Ironically Microsoft, a Progyny client, is currently trying to acquire Activision so that one might flip back. By my estimates for members, they still had 99.5% gross member retention for each of the last two years. Even if there are 4X the number of defectors than I found, 98% gross retention is still very elite.

Progyny clients typically sign three-year contracts. Pricing is negotiated per Smart Cycle treatment bundle based on several factors. The nature of this revenue being recurring is dependent on utilization remaining similar from year to year. Some Columbia MBA students presented an interesting short thesis on Progyny where they believed the pool of potential members was more like a finite resource that would be depleted over time. With high growth and lots of new clients, it’d be hard to decipher this in any aggregate data. Excluding the initial covid months where clinics briefly shut down, female member utilization has consistently ranged 0.44% - 0.47% on a quarterly basis, extremely steady. Female utilization is the best proxy for cycles and therefore revenue. While the depletion thesis is interesting theoretically and something to monitor, I believe all the tailwinds and growth trajectory completely outweigh this.

Thorndike further explains how revenue quality leads to simple operations, pricing power, and capital efficiency. Progyny would hit three check marks here. With massive growth in the past four years (8X cycles, 10X revenue), gross margins have steadily risen from 15% in 2017 to 22% in 2021. As the demand aggregator, they should continue to exhibit pricing power. The business does not take much capital beyond working capital, and annual adjusted EBITDA margins since 2017 have gone -16%, 1%, 8%, 9%, 13%. Great signs of operating leverage and efficiency while scaling.

Finally, a few other factors Thorndike mentions worth calling out. Revenue quality is also strengthened by being a B2B business that provides a service that is critical but a very low percentage of total end cost. Great, Progyny provides a B2B service and fertility represents less than 1% of total health care spend. Although not critical per se, I highly doubt any company will remove fertility benefits once they are covered.

Moat:

The main competitors for Progyny are the big national carriers such as United, Cigna, Aetna, and BCBS. In 2020, two thirds of the new Progyny clients had prior fertility coverage, and while this is down to 52% for new clients signed for 2022, most clients are still being taken from the national carriers. With fertility representing less than 1% of their total spend, they seem unwilling to retool their model and dedicate to outcomes the way Progyny has.

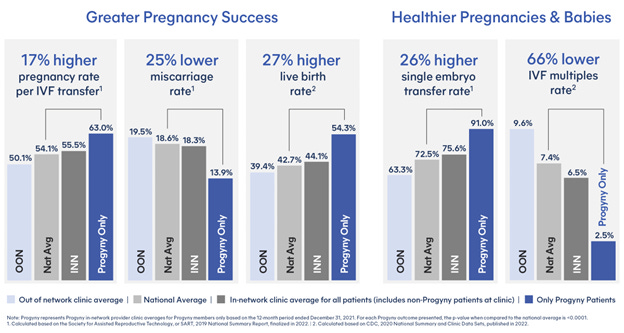

Speaking of outcomes, that is clearly a huge selling point that Progyny needs to maintain going forward. They recently published the latest clinical outcomes (see below) verified by Milliman, a health care actuarial firm. Although I dislike how they represent the data with different years, there is clear delineation in the outcomes produced by Progyny. I verified with Progyny IR that they do remove their data from the national average calculations and reweight to normalize for slight discrepancies in age distributions.

My major hang up with anointing this a strong moat business is Progyny simply operates as a middleman entity. There is nothing sophisticated about the strategies. In fact, the industry often seems to follow the innovative trends Progyny is pushing – prioritizing single embryo transfer, use of frozen embryos transfers, and chromosomal testing of embryos. Being the first mover aggregating on the demand side can be a strong position but if consolidation occurs on the clinic side (which are controlled by lots of private equity currently), it could weaken Progyny’s position.

There are numerous other venture-backed companies mimicking the Progyny philosophy including Carrot Fertility, Stork Club, and Maven Clinic. These are not integrated with the health insurance plans and therefore are offered as a post-tax benefit to employees, making them less financially enviable. Perhaps the most interesting competitor to keep an eye on is Kindbody. They acquired Vios Fertility Institute in February this year and are pursuing a more vertically integrated strategy. That acquisition gives them 26 clinics across the country (note: Progyny has access to 650 provider clinic locations). They also acquired a surrogacy agency in Chicago recently and have plans to IPO next year. Also, important to note that all three clients that I discovered which had left Progyny went with Kindbody.

Valuation:

For some concluding thought on valuation, I first want to mention TAM penetration. Progyny states that large, self-insured employers represent a potential 75 million covered lives and about $10B for 2022. So that puts Progyny at around 6% penetration by members, and slightly higher by revenue. This excludes quasi-government entities, but Progyny already has a few school systems (see their Nashville case study) and Universities (University of Texas System, Tufts, Drexel). Progyny also announced earlier this year they are trialing some offerings in Canada and depending on how that goes they have their eye on several European countries. They have many clients with locations all around the globe so this could be expanding the opportunity.

Regardless, the growth trajectory seems very solid for the next five years. It likely can’t keep the 50% annual pace it has had the last few years but a 20%+ CAGR over the next five years is certainly plausible, especially with industry cycles growing ~10% annually and Progyny continuing to gain share. The company trades at a $4.3B enterprise value (no debt) with 2023 revenue projected slightly over $1B. Assuming future EBITDA margins of just 20% (incremental adjusted margins have been running higher than that), puts Progyny at 21X 2023 EBITDA. That feels entirely reasonable given the growth trajectory and revenue quality. Granted there’s a lot of SBC removed from the adjusted EBITDA number but I’d argue that actual long term margins can be higher than 20%.

Historical Numbers:

Links For Additional Information:

Podcast with Progyny chairman David Schlanger

CBS Short Thesis Presentation

NYT article on Endometriosis

Progyny Podcast – Brewing for a Fertility Benefit

Disclosure: I own Progyny (PGNY 0.00%↑) shares. Not investment advice.