CF Industries

CF Industries

Reflections, learning, and lessons from the past

With the new year kicking off, I hope to make a stronger commitment to writing. As I described, the goal is a lifestyle of perpetual learning and compounding knowledge, which writing will greatly reinforce. What follows is a glimpse of some older thoughts (composed in late 2020) in response to a prompt - “Describe an investment that didn’t work out. What did you learn from that mistake.” I’ll then circle back at the end to lightly weigh in on recent financials for CF Industries.

I have certainly made worse financial and intellectual investing mistakes earlier in my life (ask me about the first stock I shorted, or about speculating on FDA approvals), but those are amateurish and have elementary reflections. This situation is more nuanced and has deeper insight into my development as an investor.

It took me about five years to get comfortable really investing on my own. By that time (~2013), my work in consulting had taught me about the shale revolution and the prolific growth potential for domestic natural gas production. This, coupled with residual gas from oil wells, would create a sustainable and cheap source of natural gas in the US for a long time to come. Nitrogen fertilizer is critical in agriculture and the primary cost component is the raw energy (natural gas). These fertilizers must be applied every single year (recurring revenue before I studied SaaS!) and they increase crop yields. As global populations rise, demand for these fertilizers will only rise.

Situated primarily in the US, with proximity to the cheapest natural gas supply in the world and some of the most productive cropland, is CF Industries ($CF), a major nitrogen fertilizer producer. These production facilities are very capital intensive. Perfect, I thought. The low-cost producer with a sustainable advantage in a growing industry, with high barriers to entry and stable margins, trading at a reasonable valuation. I also liked a lot of the recent management decisions, namely selling the phosphate business and buying back a lot of shares.

So in 2013 I bought some CF shares. Over the next two years they performed well, beating the market. Then in the second half of 2015 and early 2016, shares fell dramatically. I bought three more times during that time frame to quadruple my position. Margins had compressed from the prior era as Chinese producers flooded the market (North America was import dependent at the time) with supply they were losing money on, and global capacity expanded. Additionally, CF entertained one major merger attempt and pursued one takeover during this time that complicated the simplicity of the story. Company execution was quite good over this time, but the market never returned to the glory days. By late-2017, the shares had rebounded somewhat, and I started exiting, fully leaving the investment by mid-2018. My return was a meager 4% annualized, while the S&P500 was closer to 15% over that same time, so the opportunity cost was quite high.

My major takeaway was that a business model can really matter. In this instance, CF executed, not flawlessly by any means, but quite well. Even with a great operator, a commodity business can truly be at the whims of other players who do not necessarily operate in an economic fashion. Price fluctuations can often be drastic due to macro factors, and forecasting macro is very challenging and typically wasted effort. I have also witnessed these kind of trends in the memory (hardware) and frac sand markets.

Another takeaway concerns porfolio management and conviction. It is critical to research and understand a company as much as possible, obviously. But the real benefit in knowing a company deeply is in being able to reason if the moves in stock prices (either up or down) are justified based on how the long-term business prospects have changed. CF was an example where I thought I knew the business better than I did, likely because modeling the financials was relatively easy, and I had related knowledge from work experiences. Forecasting can be very difficult and assigning probabilities to a range of scenarios can help.

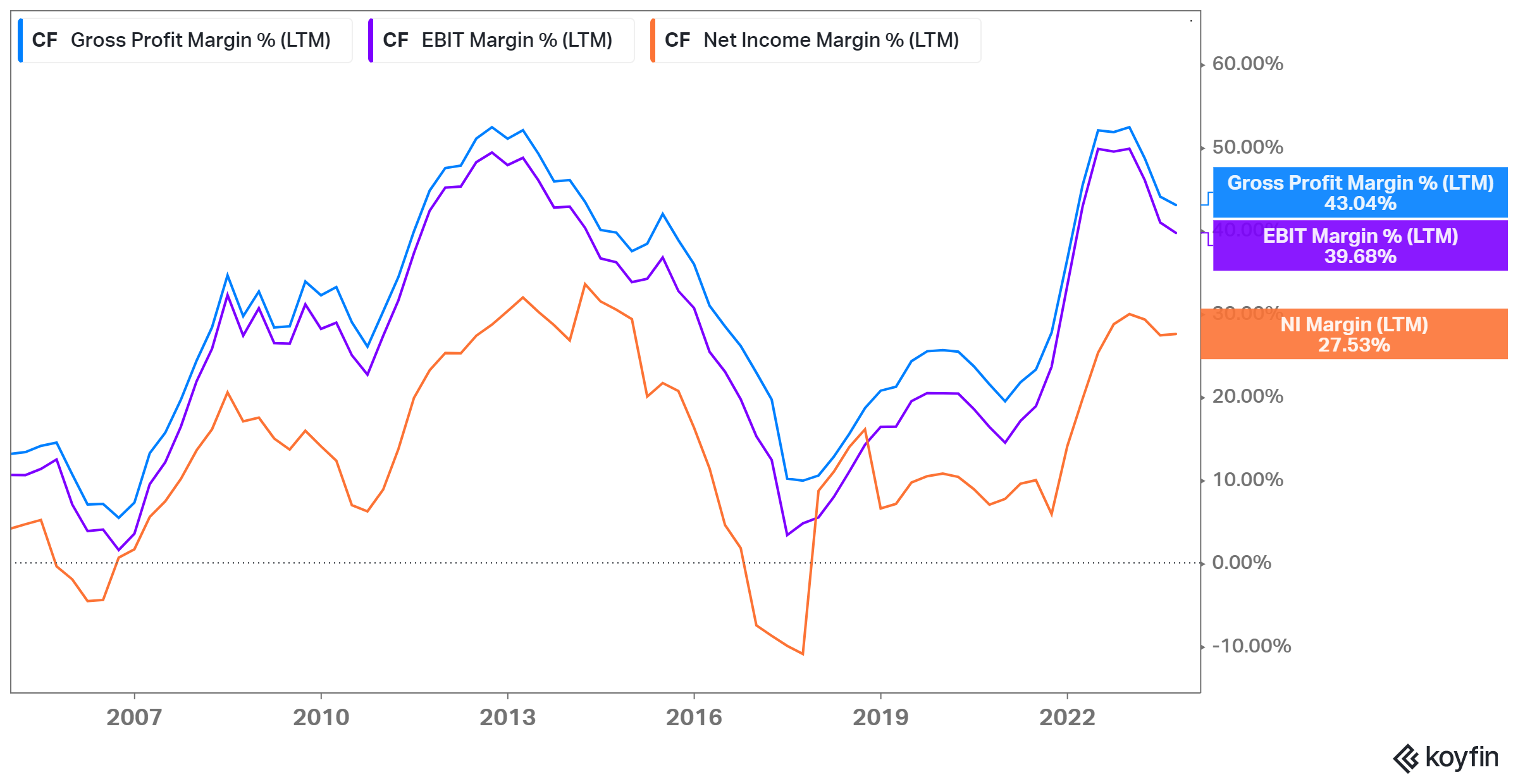

Back to current day. Below is a 20 year snapshot from Koyfin of CF trailing margins.

It’s interesting see how the 2022 cycle margins topped out nearly at the same level as 2013. Makes perfect sense that my lagging returns from 2013-2018 happened when starting from peak margins. It seems so obvious in retrospect but modeling valuations based on average margins over a longer time frame (say ~30% GM and ~15% NI in this case) is paramount for a cyclical or commodity type business.

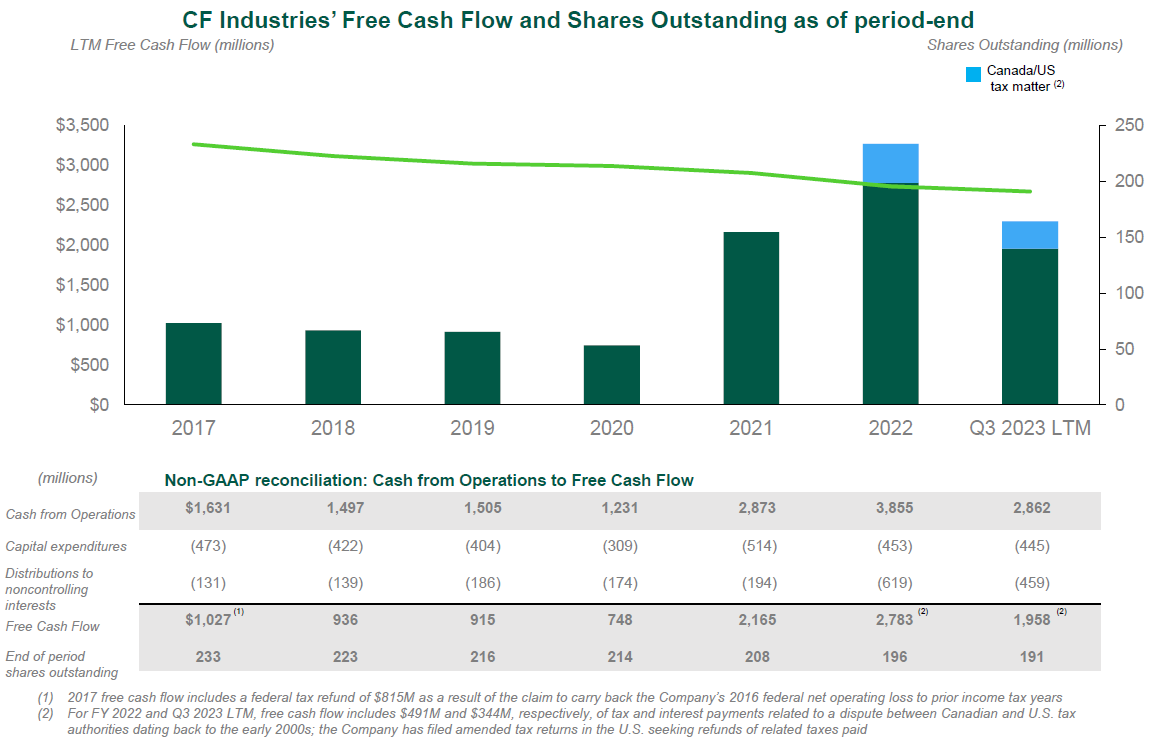

Another way to illustrate this is to look at the chart below from 2023 Q3 presentation. FCF recently has been extremely strong - $2.8B in 2022 and $2B on a TTM basis. But the average over 2017-2020 was just $906M. What projections you use going forward paints a drastically different picture for a $15B market cap company.

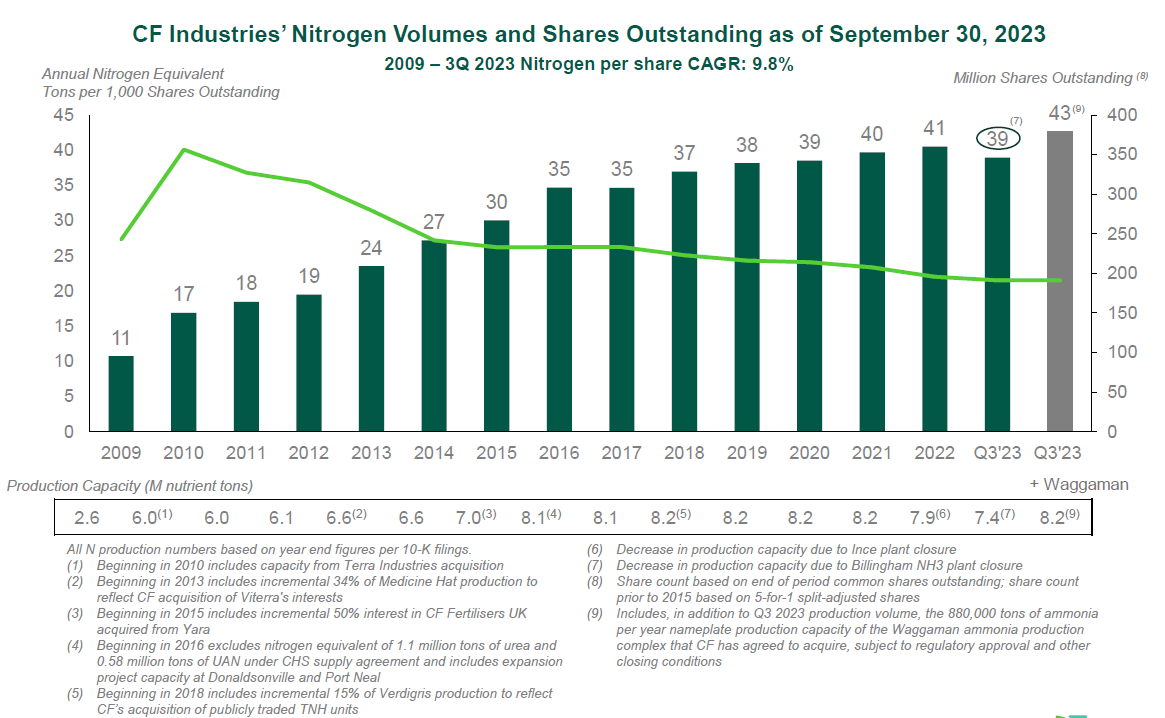

The company has grown fertilizer capacity per share at an incredible 10% CAGR since 2009, but this really came in two distinct phases. 2009-2016 saw a tripling, while 2016-present is up about 20% in aggregate. Management in recent years has ratcheted up buybacks (shares outstanding down about 4% over the last year), while net debt has been dropping significantly. It just makes me wonder if they are doing this prudently though as they seem to sync up with peak margins. They spent $100M in 2020, $539M in 2021, $1,347M in 2022, and now just $155M in the first 9 months of 2023 on buybacks. Look at the stock chart and it’s almost inverted from what would be ideal. Makes me question whether my old assessments of management were too generous.

Disclosure: Not investment advice. I am an individual investor seeking to study businesses, continuously learn, and find the best investment opportunities. The Sutherland Woods are a small piece of forested conservation land near my house.