Ballast Cannibals

As my personal investing ethos has shifted over time to a more growth centric philosophy, I have found it useful to balance the inherent volatility in those equities with some distinct core positions that act as ballast. Ones that are excellent and stable businesses, do not require continuous monitoring and research, but are more limited in their growth potential (likely won’t 10X in a decade). These can be a bit freeing mentally while helping to steady the compounding of the portfolio. Three major positions, which represent about one third of my retirement account, have evolved into what I now think of as ballast cannibals. They are Google ($GOOG), Berkshire Hathaway ($BRKB), and NVR Homes ($NVR).

Ballast is typically material used to provide stability. Most commonly this is found in boats (sail or cargo ships) to keep them from capsizing, but also is used in racecar driving for weight redistribution to optimize handling. I like to expand the metaphor a bit and picture large ballast tanks at ship bottoms as adding weight to keep the momentum going forward in addition to providing stability for the portfolio. A ship full of ballast has more mass and therefore more momentum. This makes it harder to speed up yet also harder to slow down, but it keeps everything moving forward.

Cannibals are “one that eats the flesh of its own kind” according to Merriam-Webster. I first heard this idea of cannibals referring to share buybacks from Mohnish Pabrai in a Forbes Article (link). Derived from a Charlie Munger quote, it highlights companies with strong balance sheets, reasonable valuations, and a capital return policy utilizing share buybacks. Cannibalism in this instance can be the fuel source providing ballast for the stock.

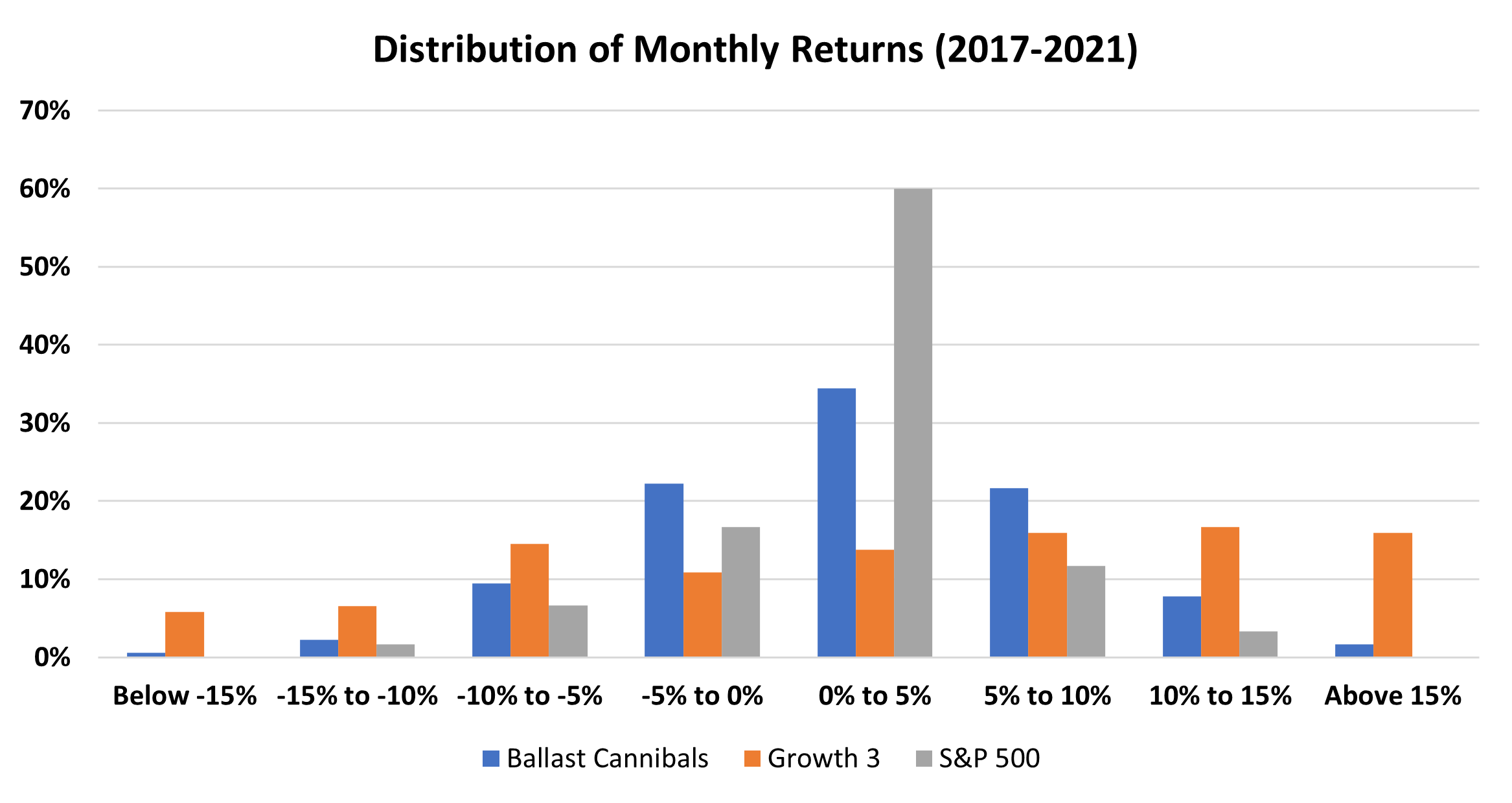

To evaluate the volatility in these ballast cannibals, I decided to compare monthly returns to the S&P 500 and a specific subset of my portfolio – call these the “Growth 3”. They are the unnamed other largest positions in my retirement account (about one third of total as well) and would be described as ecommerce/SaaS/cloud/gaming. Before compiling the data, I drew a picture of what I hoped for with gray being the S&P 500, blue being the ballast cannibals, and orange being the growth 3. This picture implies a flatter distribution for the growth 3 (more volatility) and a similar volatility for the ballast cannibals as the market, but with slightly higher returns.

The actual distribution of monthly returns since 2017 is plotted below. One of the growth 3 IPO’d after 2017 so it is not a complete 5 years of history. Nonetheless the anticipated drawing was somewhat accurate to reality as the growth 3 have a much flatter distribution curve (higher volatility!). The ballast cannibals did have slightly higher returns than the market, but it still came with a higher rate of volatility. I suppose this just goes to show that even three low beta stocks cannot substitute for an index fund.

The ideal use of free cash flow is to reinvest back into the business itself, either in things the business is currently doing or venturing into new areas. Fundamentally, these are both types of organic growth. Another use of capital for growth can be to acquire other businesses. This could be value accretive through strengthening a competitive advantage or enabling more business as a combined entity than as separate ones (1 + 1 is more than 2 sometimes). However, acquired growth can be value destructive if it costs too much, integration is unsuccessful, growth estimates are too lofty, or key management departs. When options for growth are unavailable and debt is not an overhang, instead of cash accruing, the capital should be returned to shareholders. Dividends are less than ideal because of the double taxation (corporate and individual level) so share buybacks are the preferred method.

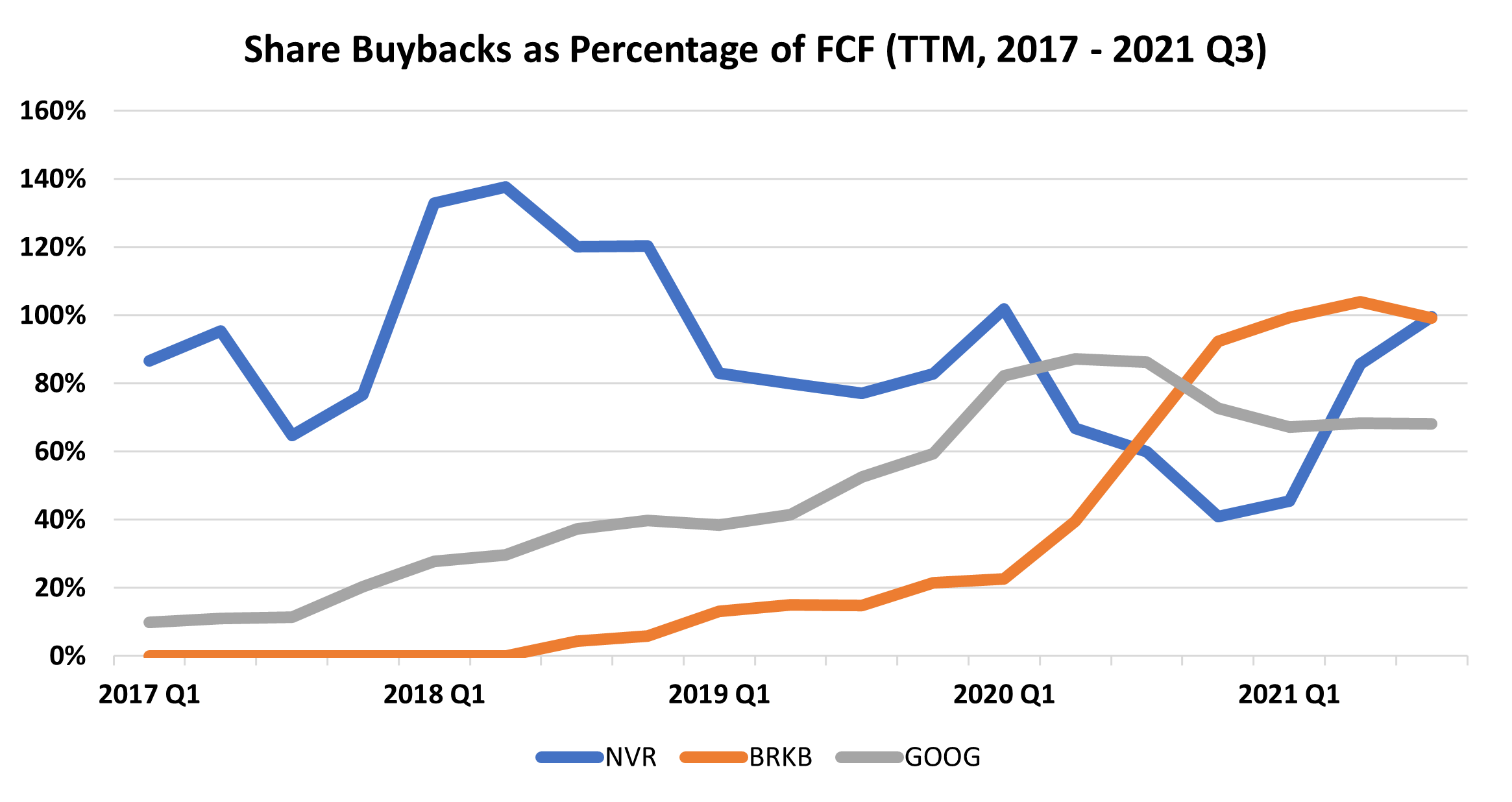

NVR is a classic cannibal as buying back shares has been a part of their strategy for a long time. As seen in the chart below, apart from a two-quarter pause at the start of the covid pandemic, they have consistently been spending 70%+ of FCF on share buybacks. Berkshire has historically used excess capital for acquiring companies – both in whole and partial equity stakes. But over the last couple years, whether through sheer internal size or unattractive opportunities, the elephant gun has been gathering dust. What started slowly in 2019 really ramped during 2020 to the point where Berkshire currently spends nearly its FCF level on buybacks. Not to mention, a big chunk of the Berkshire value is invested in Apple, which is itself a ballast cannibal. Historically, Google spent a small amount on share buybacks to help offset the stock-based compensation, but the capital allocation has changed gradually over the current management tenure since 2015. Tightening cost controls, the Alphabet division splits, and improved margins have made more cash available in recent years and management has begun to allocate more towards buybacks.

The bottom line is that these ballast cannibals are unsexy stories yet hard to lose money in for a long-term investor. To conclude, a few brief sentences on each company as to why they could be a good source of returns going forward:

GOOG: A dominant core business with growth engines from YouTube and Google Cloud that can likely maintain 15%+ revenue CAGR for the next 5 years. A fabric of innovation offers upside optionality in the “Other Bets” division. Trades currently at 26X trailing FCF and buying back 2-3% of shares annually going forward.

BRKB: Dominant core businesses (insurance, railroad, energy) with a great capital allocation strategy. Can likely maintain 5-9% revenue CAGR for foreseeable future. Trades at 23X trailing FCF and buying back 4-5% of shares annually going forward.

NVR: Unique homebuilder with extremely stable margins. New housing builds have been severely lagging demand for the past decade. Even with just 7% volume growth, 4% price growth, and share buybacks, the stock can get a 15% IRR going forward. Trades at 14X trailing FCF and buying back 4-5% of shares annually going forward.

Disclosure: Not investment advice. I own GOOG, BRKB, and NVR shares.